The Future of Investing: InSoil Green Loans and Carbon Credit Growth

How agricultural lending is creating opportunities in the booming carbon credit market

Key Takeaways

Innovative Green Investment

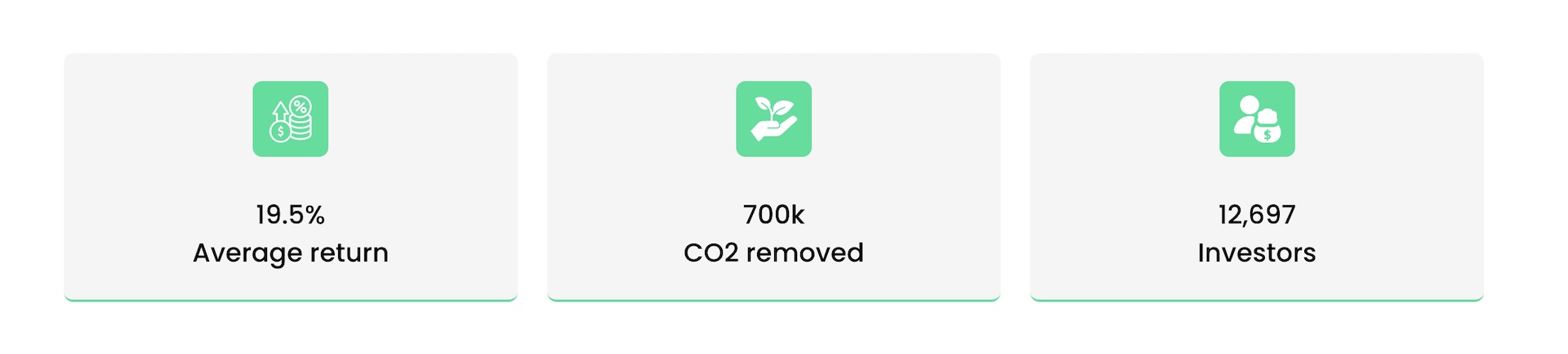

Green Loans connect retail investors with sustainable agriculture while accessing the rapidly growing voluntary carbon credit market valued at $2 billion and expected to reach $50 billion by 2030.

Superior Returns Potential

Unlike traditional 13% p.a. agricultural loans, Green Loans can deliver returns exceeding 25% annualized through carbon credit sales, with earnings paid in tranches every 2-3 years.

Robust Risk Protection

All loans are secured by first-rank mortgages on land (up to 90% LTV) and equipment (up to 70% LTV), with comprehensive due diligence and minimum guaranteed returns of EURIBOR 6M + 1.5%.

🌿Introduction to Green Loans

As global corporations intensify their efforts to reduce carbon footprints, an innovative financial platform is creating unique opportunities for investors to participate in sustainable agriculture while accessing the booming carbon credit market. InSoil, a European agricultural lending platform, has developed a novel financial instrument that promises to deliver both environmental impact and potentially high returns.

InSoil connects small and medium-sized farmers with retail investors, enabling farmers to secure funding for their operations while offering investors competitive returns.

InSoil connects small and medium-sized farmers with retail investors, enabling farmers to secure funding for their operations while offering investors competitive returns.

💚What Are Green Loans?

Green Loans are InSoil's flagship product and an excellent choice for investors seeking high returns and environmental impact. These loans are tied to the rapidly growing Voluntary Carbon Market, where companies like Microsoft, Google, and Salesforce purchase carbon credits to offset their emissions.

Unlike traditional loans, Green Loans offer returns that extend beyond the repayment period. Investors receive earnings in tranches every 2-3 years, reflecting the farm's carbon credit generation. This unique structure aligns investor returns with the success of the farmer's sustainable practices and the global carbon credit market.

Moreover, farmers benefit from 0% interest rates on these loans, improving their ability to meet principal repayments and ensuring financial stability.

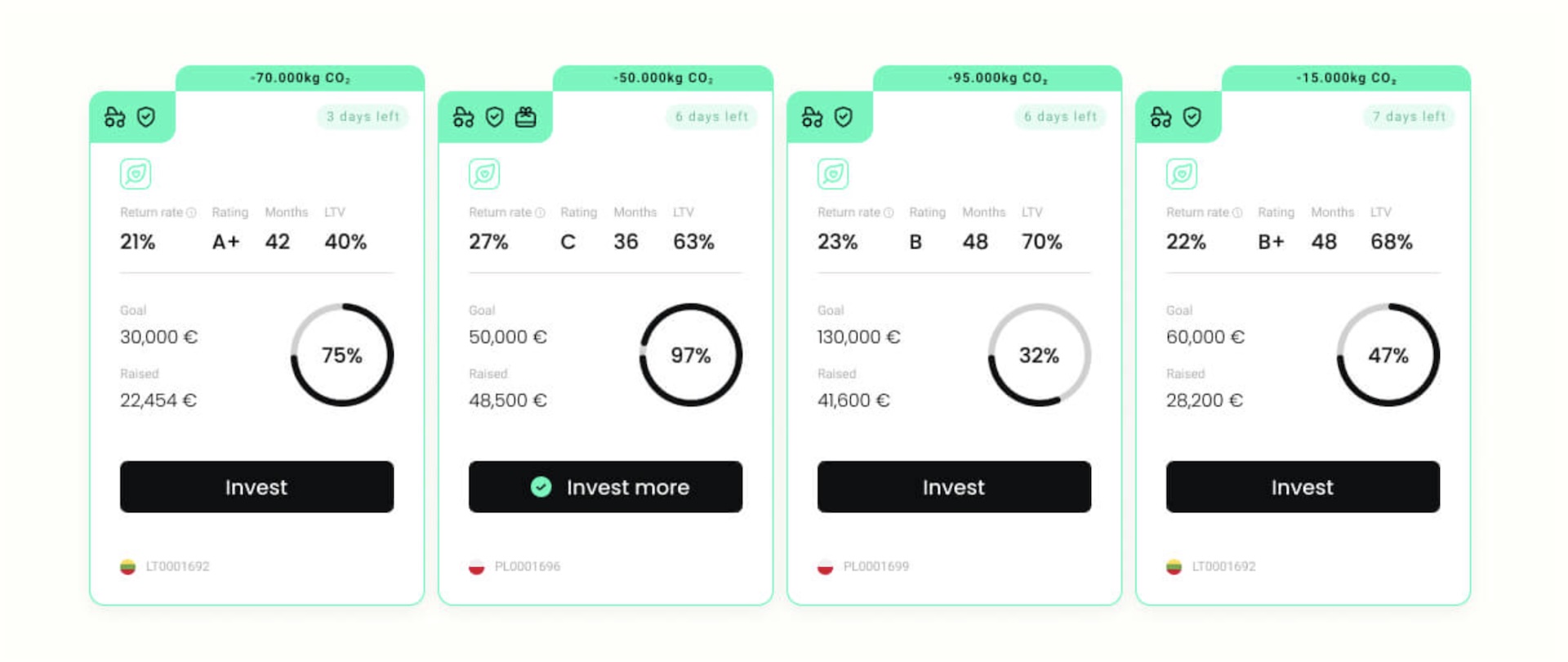

Here's how Green Loans work:

Purpose: Farmers receive Green Loans to adopt sustainable practices that generate carbon credits.

Returns: Investors earn returns from the sale of carbon credits, which are expected to increase in value as demand grows.

Expected Returns: While typical loans on InSoil generate average returns of 13% p.a., Green Loans offer even higher returns—sometimes exceeding 25% annualized—due to the potential carbon credit volume and market appreciation.

Collateralized Structure: Loans are secured with first-rank mortgages on land (up to 90% LTV) and heavy equipment (up to 70% LTV).

Zero Interest for Farmers

Farmers benefit from 0% interest rates on Green Loans, improving their ability to meet principal repayments and ensuring financial stability.

🌍The Carbon Credit Connection

What makes these loans particularly interesting is their connection to the Voluntary Carbon Market. It has seen significant growth in recent years, with major tech giants like Microsoft, Google, and Salesforce actively purchasing carbon credits to offset their emissions. Agricultural carbon credits, generated through sustainable farming practices, have emerged as a particularly valuable segment of this market. These credits are created when farmers implement methods that reduce carbon emissions or sequester carbon in the soil. Each carbon credit represents one metric ton of carbon dioxide (or equivalent greenhouse gases) that has been reduced, avoided, or removed from the atmosphere.

The Voluntary Carbon Market emerged as a response to growing concerns about climate change and the need for mechanisms to offset carbon emissions. Unlike compliance carbon markets, which are tied to mandatory emissions reduction schemes like the European Union Emissions Trading System (EU ETS), the VCM operates on a voluntary basis, allowing companies to purchase carbon credits to compensate for emissions they cannot reduce internally.

Analysts predict that the market could grow from a value of around $2 billion in 2021 to $50 billion or more by 2030, driven by increased demand from corporations and the rising price of high-quality carbon credits.

📊Key Investment Features

Return Structure

Returns are paid in tranches every 2-3 years after loan issuance

The earning period extends beyond the loan term (loan period plus one additional year):

60% of income received during the loan period;

40% of income received for the following year after the loan period.

Risk Mitigation

All loans are secured by first-rank mortgages on assets

Comprehensive due diligence process for farmer selection

Personal liability of farm owners

Regular monitoring and support from InSoil's agronomy team

If the project fails to be delivered successfully through no fault of the farmer, the farmer commits to paying investors a minimum interest rate of EURIBOR 6M + 1.5%. This commitment applies in situations such as the lack of market demand for selling carbon credits, among others.

🛡️Investor Protection Measures

InSoil takes several robust measures to protect its investors and ensure their funds are secure. The first layer of protection comes from a strict loan selection process. Every loan application is rigorously assessed to evaluate the borrower's financial health and risk level. Farmers are required to provide comprehensive financial documentation, such as balance sheets, tax declarations, and farm certifications. The platform also conducts an in-depth analysis of the borrower's operational history, ensuring that only farms with at least two years of activity and strong financial metrics, such as adequate debt-service coverage and equity ratios, are considered.

Collateral is another critical safeguard for investors. InSoil accepts only first-rank mortgages on pledged assets, including agricultural land and heavy equipment. These assets are carefully evaluated to ensure their value sufficiently covers the loan amount. For equipment less than five years old, the platform requires comprehensive insurance policies that list InSoil as the beneficiary, offering additional security in case of damage or loss. The use of first-rank mortgages further prevents the borrower from selling or leasing the pledged assets without permission.

In the rare event of default, InSoil takes decisive action to protect investors' interests. Contracts are terminated after 90 days of non-payment, and the collateral liquidation process is initiated. InSoil manages this process through an in-house recovery team, supported by legal experts when necessary. The platform prioritizes out-of-court settlements or loan restructuring when possible to expedite recovery, but if these options are unfeasible, it proceeds with collateral sales to ensure investor compensation.

Market Growth Potential

The Voluntary Carbon Market is predicted to grow from $2 billion in 2021 to $50 billion or more by 2030, driven by increased corporate demand for carbon credits.

Guaranteed Minimum Returns

If the carbon credit project fails through no fault of the farmer, investors are guaranteed a minimum interest rate of EURIBOR 6M + 1.5%.

Advantages

- ✓Returns potentially exceeding 25% annualized

- ✓Backed by first-rank mortgages on land and equipment

- ✓Access to growing carbon credit market

- ✓Environmental impact through sustainable agriculture

- ✓Minimum guaranteed returns of EURIBOR 6M + 1.5%

- ✓Comprehensive due diligence and farmer selection process

Considerations

- •Returns paid in tranches every 2-3 years (not immediate)

- •Dependent on carbon credit market performance

- •Earning period extends beyond loan term

- •Agricultural sector exposure risks

Conclusion

InSoil's Green Loans represent an innovative approach to agricultural finance, one that could help accelerate the transition to sustainable farming practices while offering investors access to the growing carbon credit market. As the voluntary carbon market continues to expand and sustainable agriculture gains importance, such financial innovations may play an increasingly significant role in shaping the future of agricultural investment.

Start Investing in Green Loans

Join the sustainable agriculture revolution and access the growing carbon credit market with InSoil's innovative Green Loans.

Explore InSoil