7Harvests Review 2026: A Promising New Swiss P2P Platform?

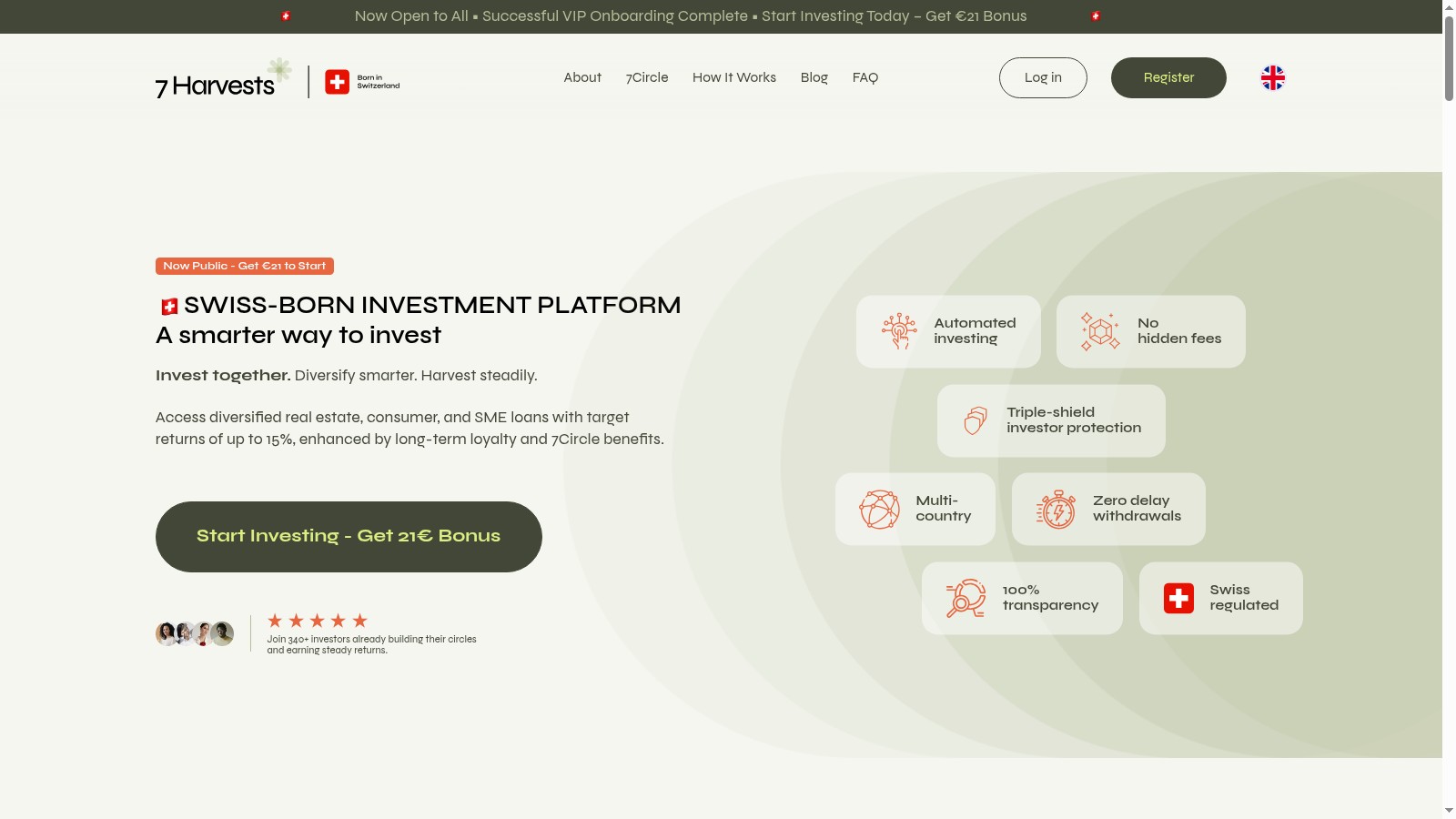

7Harvests combines project returns of up to 15% with Swiss governance, diversified loan types and up to 4% extra through its loyalty and referral programme.

The short version

- What it isA newly launched Swiss crowdlending marketplace presenting loan exposure across consumer-credit, SME and real estate categories. 7 Harvests AG is based in Zug, while the platform is aimed primarily at Swiss residents and may accept some international investors.

- Headline offerThe website advertises project returns of up to 15%, a €50 minimum, no investor fees, manual and automated investing, segregated accounts and two layers of buyback protection. Qualifying 7Circle loyalty and referral bonuses can add up to 4% extra.

- What stands outThe founder has previous P2P experience through Hive5, the company names its board and compliance function, and it has published audited financial statements rather than providing only limited corporate information.

- What to keep in mind7Harvests is still at the beginning of its public track record. Investors should therefore start gradually, diversify across loans and follow the platform's developing performance statistics.

- Would I sign up today?Yes — with a small, diversified test allocation. The €50 minimum makes that easy, and I would increase only after seeing repayments and completing a withdrawal.

This is a research-based first review. I have not yet completed a full investment and withdrawal cycle on 7Harvests, so the returns below are platform figures rather than my personal results. Based on the product, team and legal structure, I like the platform. The offer is simple, the €50 minimum is accessible, and the people behind it have relevant P2P experience.

What 7Harvests is in 2026

7Harvests presents investment exposure across consumer-credit, small-business and real estate loan categories in several countries. Investors acquire assigned claims under loans arranged through the platform. 7Harvests then administers payments, represents investors during collection and acts as collateral agent when security is attached to a loan. It is an intermediary, not a bank.

The operator is 7 Harvests AG, registered in Zug under CHE-356.409.118. The company was incorporated in April 2024 as Toucan Technology Solutions AG and renamed 7 Harvests AG in March 2026. Its founder and chairman, Ričardas Vandzinskas, previously co-founded and led Hive5. The current Swiss board also includes Kurt Schöllhorn.

Founder Ričardas Vandzinskas previously co-founded and led Hive5 before launching 7Harvests.

The wider team also lists previous experience at SEB, Danske Bank, Barclays, Debitum, Hive5 and Bondora. For a new platform, that background matters: the team is not learning lending and P2P operations from zero.

Availability is currently focused on Switzerland. The General Terms say the service is primarily directed at Swiss residents, although investors from other eligible countries may also be accepted subject to local rules. US citizens are excluded.

Returns, fees and how investing works

The basic workflow is familiar: complete identity verification, deposit EUR, select loans manually or configure auto-invest, then receive interest and principal into the platform balance. Interest is normally paid monthly unless a listing specifies another schedule. Public material describes terms from roughly 6 to 60 months.

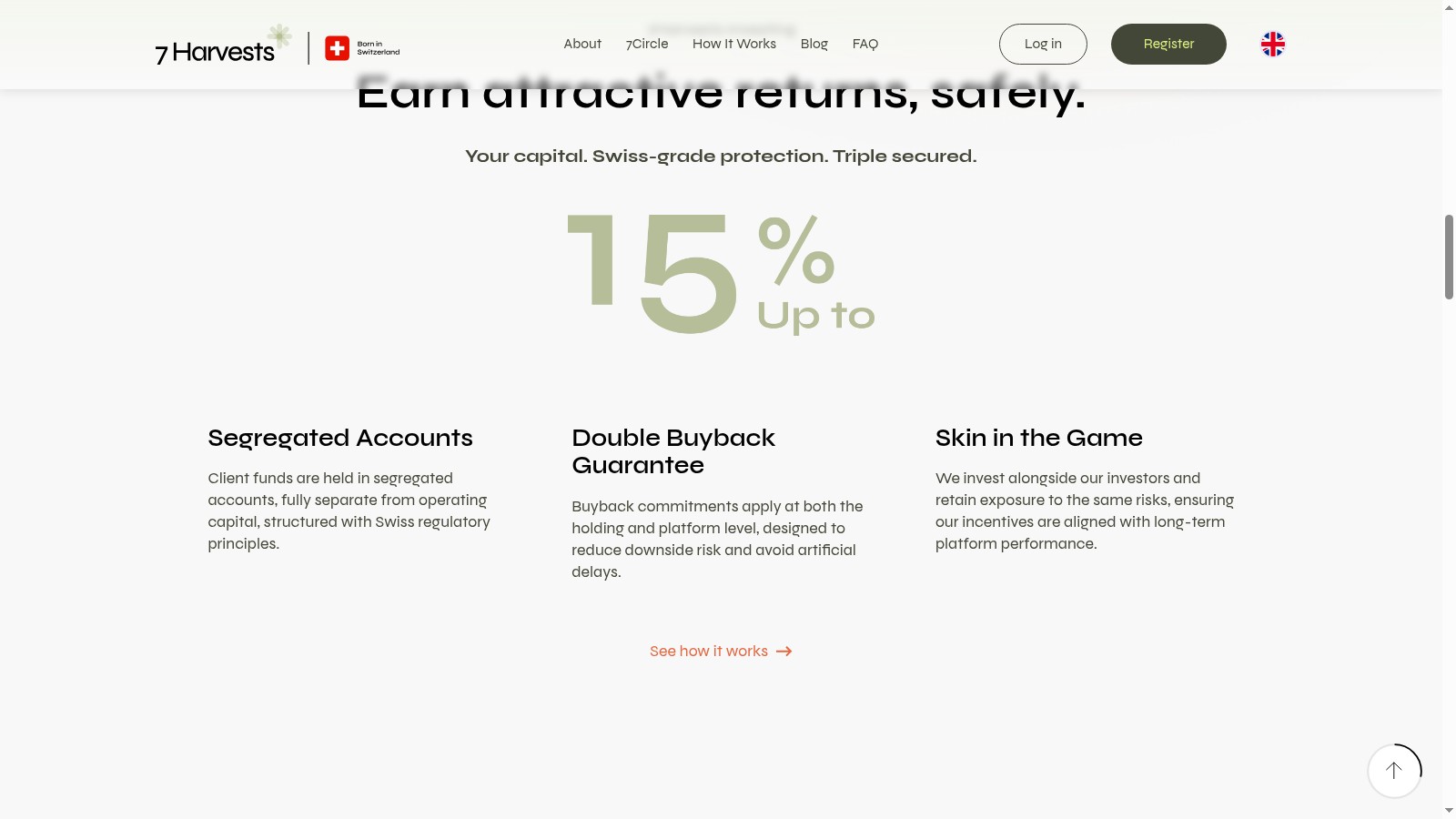

The public offer is straightforward: investors can start from €50, project returns reach up to 15%, and both manual selection and auto-invest are available. Qualifying investors can add up to 3% through the 7Circle loyalty programme and another 1% through referrals, taking the advertised promotional maximum to 19%. The actual project rate, duration, repayment schedule and protection are shown before investing.

The platform does not advertise an investor commission for deposits, investments or withdrawals. External banks and payment providers may still charge transfer or currency-conversion fees. Uninvested cash can be withdrawn to the verified bank account, but active loans should be treated as held to maturity.

The terms provide a legal framework for a secondary market, but I would still plan to hold investments until repayment. That is how I approach most P2P loans, regardless of whether an exit feature exists.

The 7Circle programme can add up to 3% for investors meeting its loyalty thresholds, while the referral programme can add another 1%. That produces a maximum combined uplift of 4%, although eligibility depends on the relevant balance and referral conditions. I would compare projects using their base rate first and treat the bonus as an extra.

Is 7Harvests safe?

7Harvests combines borrower assessment, originator buyback and a second platform-level protection layer.

Segregated accounts

7Harvests says uninvested client money is held separately from operating capital. This is useful protection while cash is waiting to be invested. It does not protect money already transferred into a loan, which remains exposed to the borrower, originator, collateral and servicing structure.

As with other P2P platforms, client balances are not covered by deposit insurance. The important point is that uninvested money is segregated from operating capital, which is the structure I want to see.

Buyback and recovery

Under the General Terms, the loan originator must buy back a claim after the underlying borrower is more than 60 days overdue, including accrued interest. Separately, 7Harvests advertises a second platform-level protection layer. The platform also states that it maintains a minimum 10% cash-to-portfolio ratio from its own operational liquid capital to support that commitment.

The originator is contractually required to buy back a claim after more than 60 days of borrower delay. Separately, 7Harvests advertises a second platform-level protection layer. I like the two-level structure, but investors should still review each project's documents because the precise scope and funding of the second layer matter.

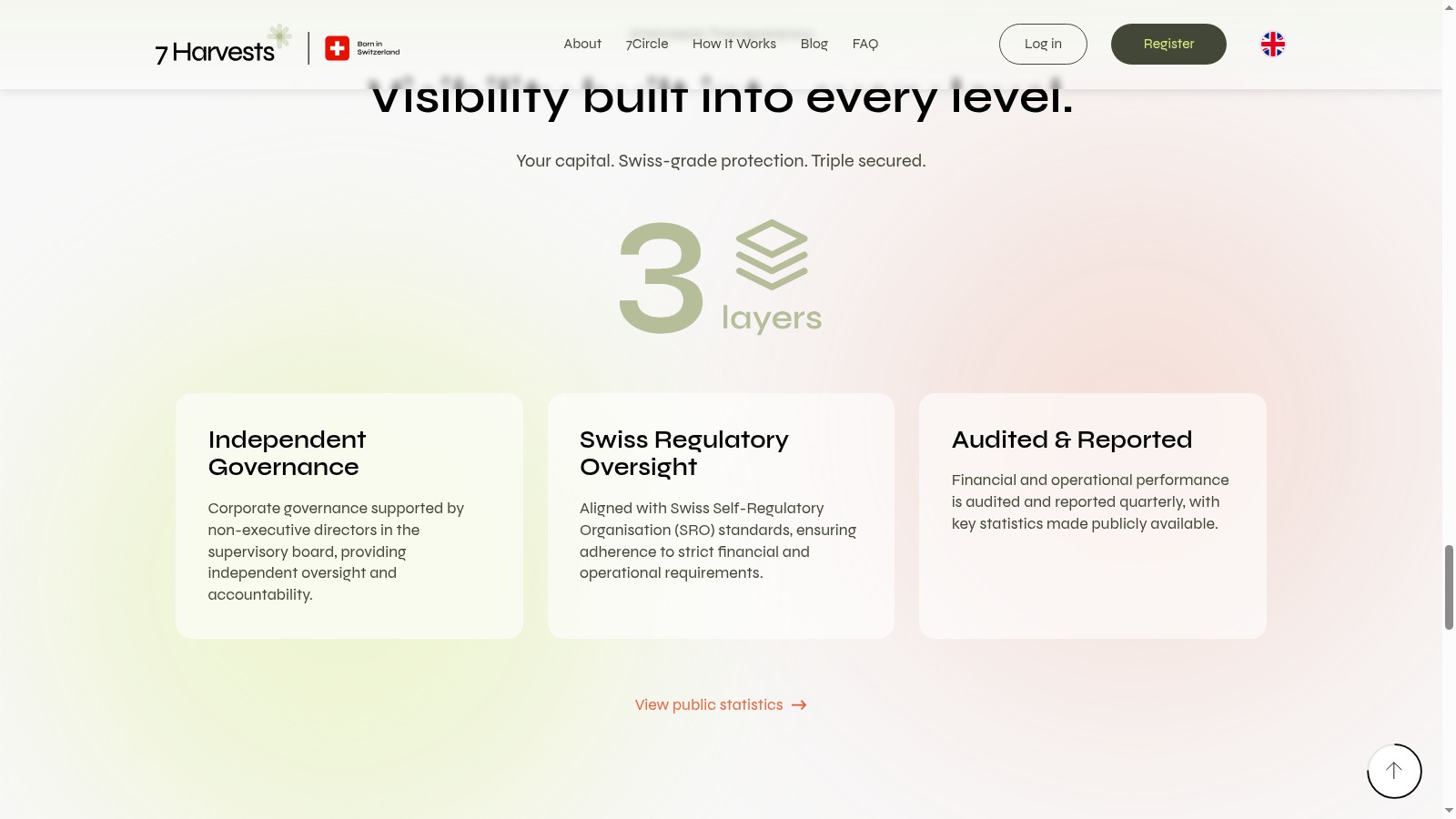

Regulation and governance

The governance structure combines a Swiss company, named board, AML controls and published audited financial statements. 7Harvests states that its application for VQF SRO membership is in progress.

The current footer and FAQ state that the application for VQF SRO membership is in progress. The General Terms still refer to active VQF supervision, so that document should be updated to match the platform's current public status.

VQF supervision primarily covers anti-money-laundering compliance. FINMA explains that SRO membership is different from direct prudential supervision. 7Harvests publishes its company, board, AML function and audit information publicly, which is more disclosure than I usually see from a newly launched platform.

The published financial statement

7Harvests publishes audited financial statements, which is unusual for a platform at this stage. The audited statement covers the predecessor entity through 31 December 2025, before the 7Harvests name and public launch. It is a pre-launch snapshot, not a report on the current operating platform.

At that date, the company reported CHF 17,405 in assets, CHF 12,305 in equity, no operating revenue and an annual loss of CHF 87,695, alongside an auditor's note concerning the company's capital position. This is not unusual for an early-stage technology business before commercial launch. The next useful document will be a post-launch balance sheet showing the capital behind the operating business and its second protection layer.

7Harvests vs established alternatives

The most useful comparison is not which platform advertises the highest rate. It is what evidence exists behind each marketplace.

| Platform | Strongest use case | Main trade-off |

|---|---|---|

| 7Harvests | Early access to consumer-credit, SME and real estate exposure in one Swiss structure | Track record is still developing following its recent launch |

| Mintos | Large, regulated marketplace with broad originator diversification | More complex products and meaningful historical originator defaults |

| Debitum | Regulated business-loan exposure | Smaller marketplace and concentration in a limited number of originators |

| EstateGuru | Property-backed loans with a long operating history | Illiquidity and a substantial legacy recovery portfolio |

Mintos, Debitum and EstateGuru have more historical data. 7Harvests has a lower entry point than many real-estate platforms, three loan categories and a team that already knows the P2P market. I see it as a small diversifying allocation alongside established platforms, not a replacement for them.

Pros and cons

Pros

- Consumer-credit, SME and real estate exposure through one marketplace

- Manual selection and automated investing tools

- No advertised commission for investing, deposits or withdrawals

- Named Swiss company, board, AML officer and published audited financial statements

- Segregation of uninvested client funds from operating capital

- Founder has previous experience building a European P2P platform

Cons

- Short public track record because the platform launched in 2026

- VQF and Swiss SRO status needs one consistent update across the website

- Second buyback layer has not yet been tested through a full credit cycle

- Public volume and repayment statistics are still limited

- No established secondary-market liquidity yet — plan to hold to repayment

FAQ

Is 7Harvests regulated?+

What is the minimum investment on 7Harvests?+

What return does 7Harvests offer?+

Does the buyback guarantee make 7Harvests safe?+

Can investors outside Switzerland use 7Harvests?+

Verdict

7Harvests is a strong launch. The product is easy to understand: start from €50, choose exposure across consumer-credit, SME or real estate categories, earn project returns up to 15%, and use manual selection or auto-invest. Qualifying loyalty and referral bonuses can add up to 4% extra. The founder has already helped build a European P2P platform, and the Swiss company publishes more governance information than most new platforms.

I have not completed a full investment cycle yet, so I am not assigning a personal return or long-term rating. The missing piece is time: repayments, recoveries and withdrawals need to build the track record that the product itself already suggests.

Would I sign up today? Yes — with a small, diversified allocation. I like the €50 entry point, the mix of loan types and the two-level buyback structure. If 7Harvests follows this launch with clear portfolio statistics and consistent execution, it can become a serious part of a European P2P portfolio.

You can explore the current investment opportunities directly on 7Harvests.

Keep reading

An honest Stock.estate review based on my own investing — an ECSPR-licensed Romanian real estate crowdfunding platform with up to 20% returns, mortgage-backed collateral, a €100 minimum, and zero investor fees.

An honest Viainvest review based on 2+ years of personal investing — Latvian licensed P2P platform with strict 60-day buyback guarantee, my actual 11.83% net yield, and how it fits alongside Mintos in a diversified P2P portfolio.

An honest Ventus Energy review — Latvian platform that finances wind, solar, and biogas energy projects across Europe with bond-like investor returns. The structural model, real returns, regulatory tailwinds, and how it fits in a European real-asset portfolio.

An honest Twino review based on 5 years of personal investing — Latvian P2P platform with €1B+ in loans funded, my actual 10.94% XIRR-calculated return, and the structural model that's worked through the 2020-2022 P2P consolidation.

An honest Triple Dragon review — UK-based platform that finances mobile-game intellectual property and shares revenue with retail investors. The structural model, the realistic returns, the tail risks, and how it fits in a diversified European portfolio.

An honest Trading 212 review for UK and European investors — the ISA wrapper that makes it the UK retail default, free trades that are genuinely free, the safety record after 20+ years, and where it stops being the right answer.